Most founders treat budgeting as a spreadsheet exercise.

In reality, budgeting is a decision-making system, and decision-making is driven by psychology.

After working with dozens of companies on budgeting and FP&A, I have seen the same behavioral patterns derail plans again and again. This article explains the most common budgeting biases and the practical fixes that make budgets work in real life.

What is corporate budgeting?

Corporate budgeting is the process of planning revenue, expenses, and cash flow for a future period, whether monthly, quarterly, or annually. A good budget is not only financially accurate, it is designed so teams can actually execute it.

Why does psychology matter in budgeting?

Because budgets are created by people.

Leadership teams, managers, and employees respond to incentives, uncertainty, fear of missing targets, and internal politics. These human factors influence forecasts, cost assumptions, and resource allocation, often more than the numbers themselves.

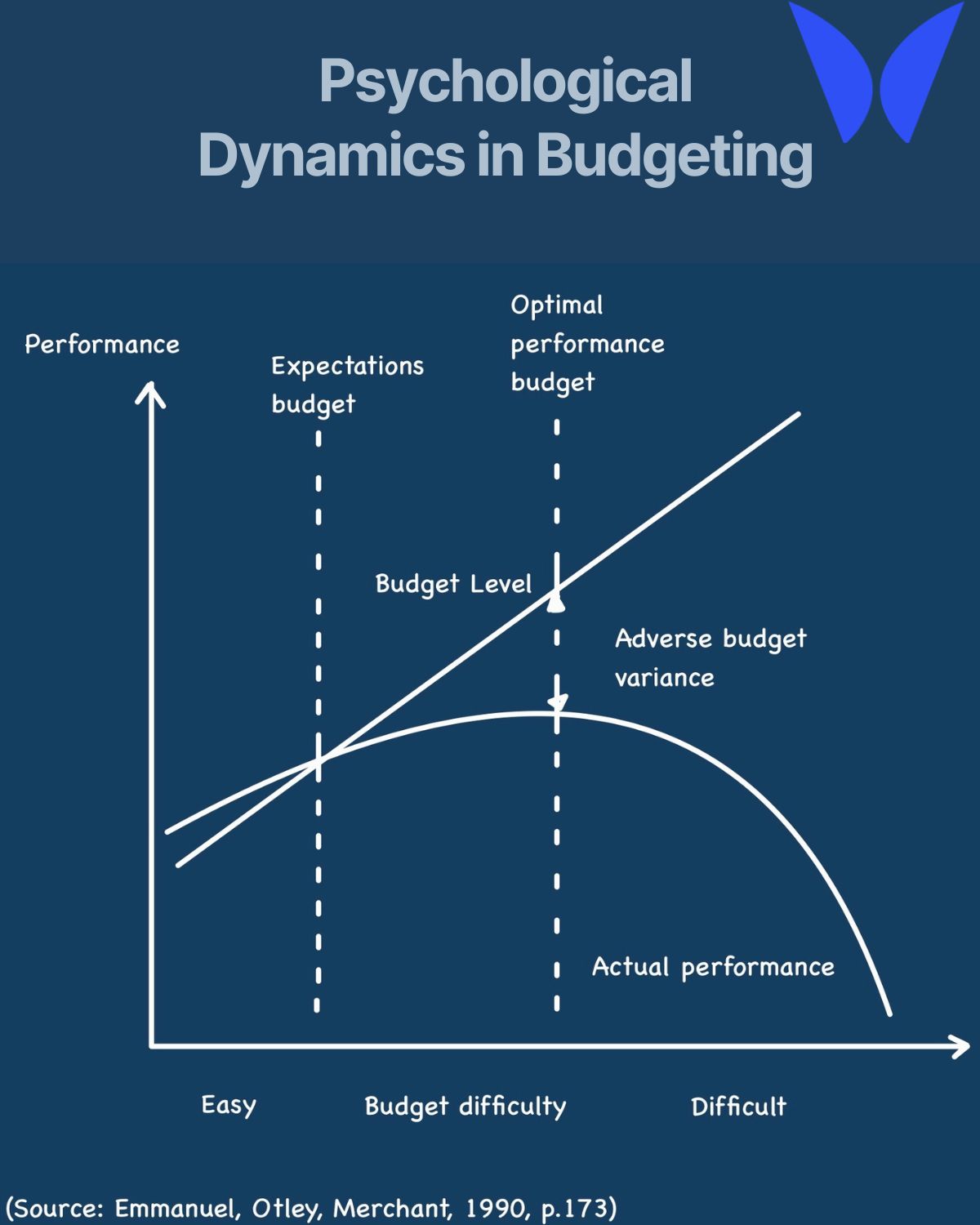

Why do budget targets demotivate teams?

The problem, overconfidence creates unrealistic targets

Cognitive biases, especially overconfidence and optimism bias, often lead leadership teams to overestimate revenue and set targets that feel unattainable.

When targets are imposed top down and do not match operational reality, teams disengage. Motivation drops, ownership fades, and execution suffers.

The solution, set targets in the stretch but achievable zone

To increase motivation and accountability, targets should be ambitious yet credible. Managers should be involved in target setting to combine bottom up insight with top down strategy. Targets must also be linked to performance metrics and financial incentives that reinforce execution.

Using historical performance and pipeline confidence helps avoid hope based budgets.

Why do departmental budgets inflate every year?

The problem, hidden buffers inflate the total budget

Departments tend to add contingency buffers at the line item level. Individually these buffers appear reasonable, collectively they inflate the total budget and reduce capital efficiency.

This dynamic is driven by uncertainty and defensive planning, not bad intent.

The solution, create one centralized contingency reserve

Instead of allowing buffers inside every department, contingency should be removed at the business unit and expense level. A single explicit contingency reserve should be created at company level and sized using historical variance, for example last year’s budget versus actual delta as a percentage.

This preserves flexibility without encouraging fear driven padding.

What is the sunk cost fallacy in budgeting?

The problem, past spend keeps bad projects alive

The sunk cost fallacy is the tendency to continue funding a project because of past investment rather than expected future returns.

This leads to capital being locked into underperforming initiatives while higher potential opportunities remain unfunded. Strategy becomes about defending past decisions instead of investing in future value.

The solution, evaluate decisions based on future ROI

Projects should be reviewed using a forward looking framework based on expected return on investment. Past spending should be treated as irrelevant.

Regular resource allocation reviews, ideally on a quarterly basis, help ensure capital flows to the most valuable opportunities. If you would not approve a project today, it should not continue to receive budget.

The takeaway, the best budgets are behavior aware

A budget that ignores psychology will fail even if the math is perfect.

A budget that accounts for human behavior improves execution, increases ownership, reduces waste, and allocates capital to what actually drives growth.

Frequently asked questions about budgeting psychology

Is budgeting part of accounting or finance?

Budgeting typically sits within finance and FP&A because it is forward looking and supports planning, decision making, and capital allocation.

How do you create realistic budget targets?

Realistic targets are created using historical trends, pipeline quality, scenario planning, and manager input. The goal is to stretch performance without destroying credibility.

What is a contingency reserve in budgeting?

A contingency reserve is a centralized budget allocation designed to absorb uncertainty and variance, and it is more effective than hidden buffers inside departmental budgets.

How do you avoid the sunk cost fallacy in financial planning?

You avoid the sunk cost fallacy by evaluating decisions based on future returns, reviewing projects regularly, and defining clear stop or continue criteria in advance.

Subscribe to receive the latest blog posts to your inbox every week.